"selling books to selling everything" seemed a reasonable change to me, and I think it was articulated as a strategy by bezos early on. As you say, books were a starting point.

Selling books to selling computing on demand... That was a big leap, and the most profit generating "pivot" I can think of.

Alexa, video streaming, kindle and ono...these are really Amazon becoming like Google. They're now defined as a business by the skills/abilities they have, not the services they provide. Technology company, not search company.

..this justifies investing more on self driving cars or nuclear power and less on search engines. For most companies this would just be pr/hr-speak, and impossible in practice. Usually companies have to spend most of their money on core products, because it takes money to deliver those products. Tesla or Walmart could define themselves however they want, but they'll never be able to spare more than a penny or two of car dollars on stuff that isn't related to making cars. The margin isn't there.

To be a Google, you need a legitimate cash cow. Amazon now have one, aws.

A lot of what Google does, or fails at, makes a lot more sense when you actually think about what its core competencies are: big data, anything that works best with an exabyte of data, a billion CPU-years, and some crazy machine learning / good ol' fashion statistical elbow-grease.

It's obvious how this relates to their original business, Search, and how it relates to their more successful spin-offs and their failures. Spam filtering and self-driving cars are more big data problems (though spam filtering is less impressive nowadays), and the Cloud and YouTube make a lot more sense when you realize that Google already runs a really efficient data-center. Meanwhile, eg, Google Reader was something that didn't really need a Google to run, and suffered for it.

It's not as obvious to me how AWS grew out of Amazon; it doesn't seem obvious to me that you need that much data center to run Amazon (or at least, Amazon-at-that-time).

I wish I'd said it like that. Surprising, for just that reason.

Your Google point (besides being a contrast to amazon's surprising athena) is an interesting way of describing things.

Youtube, Android and even adwords & web analytics were bought fairly formed, and clearly were quite good already. That's a skill in itself. When you think of examples of ebay, skype and how few buy-outs really do succeed like that.

Google could make the web work too. Remember how slow yahoo a basic webmail service was. The idea that they'd make an excel that worked.. it wasn't trivial.

But I think you're right on the lead skill. If it works best with an exabyte of data, a billion CPU-years... it works best on a google.

I think that is an interesting insight - the majority of Google's offerings are from aquisitions of 'established' implementations, whereas Amazon's are developed in-house to solve a pain-point, that is felt by other businesses, too.

So, is Amazon really more B2B, while Google is B2C?

Is Amazon using e-commerce like a US university looks at undergrads for funding?

Google has bought a number of companies, yes (Google Maps is another piece that started as an acquisition) but I'd note that which acquisitions survive and thrive also relates back to the core competencies.

Stage 1: Railroads are going to be the next big thing. Smart play: Be one of the first with a railroad.

Stage 2: Everyone knows railroads are the next big thing. Tons of people are raising money to build railroads. Smart play: Sell those people the stuff to build railroads.

Stage 2: make it easy for everyone to have a railroad by leasing them yours. Lease yours multiple times over, each time for less than it would cost the customer to build a new one.

Stage 3: everyone has a railroad which they rent from you. Collect rent on all railroad activity forever.

So now - what is Stage 3; once everyone has a railroad - then what?

Then it's a long time after the initial Industrial Revolution, and you're in a fantastic world where it's commonplace for ordinary people to own a steel machine which can travel as fast as a train at "high speed."

I don’t know where the metaphor is supposed to go, but I’d imagine that the next stage for AWS is to move further into SaaS products, and to introduce new products and features that lower the engineering overheads of operating on AWS.

So much this. A commerce company needs peak compute in December and tax companies in March, so why not share server farms? If you extend that idea to a business model, you make a normally internal cost center into an external facing revenue generator.

I recall an episode of Software Engineering Daily where the host, Jeff was interviewing some Microsoft guys and they suggested AWS was the result of Amazon selling it’s own infrastructure. Jeff interrupted him and said that was “not accurate.” Sorry I don’t have link to the episode here but it was not a very good one. The Microsoft guy responded by saying the truth of the story didn’t matter, which is pretty absurd but I think reflects how Amazon came to dominate the public consciousness. The truth just doesn’t matter in advertising or in reputation. We’ve learned how to undermine it with buzz and mediation.

For example, many were sick of Wal-Mart. Was it because of the way they treated their workers? No. If it were, they wouldn’t have ran to Target and Amazon instead. The actual shopping behaviors are guided by convenience but judtified by cultural associations. Target capitalized on the same image appeal without offering anything new at all. Amazon is, culturally, Target + Silicon Valley. Ad agencies all understand this very well. Amazon is neoliberalism in the flesh. There’s nothing a bit surprising about it.

What I assume is being referred to is the story that AWS got started to sell Amazon's spare compute capacity. Werner Vogels has publicly stated that this is a myth: https://news.ycombinator.com/item?id=8658383

I've always wondered about how Target can maintain this image as some kind of forward-thinking retailer when they're no better than Walmart is on most of that stuff, but I think the answer is honestly mostly "the Wrong Kind of People shop at Walmart."

They offer better service and selection in many areas than Walmart. This is particularly true outside of the south, where Walmart is just better for some reason. Here in the northeast, Walmart is like DMV especially when benefit checks come in.

They also appeal more to women, and eschew product categories that men and poor folk flock to like car parts, guns, fishing, Jesus books, crafting, etc.

> They also appeal more to women, and eschew product categories that men and poor folk flock to like car parts, guns, fishing, Jesus books, crafting, etc.

Target does not eschew most of those categories (guns and car parts are the only ones I think they consistently don't carry). Also, as an aside, crafting isn't a “men and poor people” category, anyway, but a famously huge interest for middle class women.

I live in Massachusetts. My experience is that the selection is smaller and more expensive but the goods are not of a higher quality (especially if you have a Walmart Super Center). But I think the "especially when the benefit checks come in" aside illustrates exactly what I am talking about.

For me it's as simple as making it so the stores don't look like they've been through a looting riot recently. I still go to Walmart sometimes, but I'm generally not happy about it.

> Jeff interrupted him and said that was “not accurate.”

Not accurate to say that Amazon is selling its own infrastructure, or not accurate to say that they had the internal competencies to launch AWS due to building their own infrastructure? I've always assumed it's the latter -- AWS is an abstraction of tools they needed to build anyway -- rather than literally sharing compute etc. with Amazon services.

I think this was some lazy paraphrasing on my part. I’m pretty sure the latter is what they meant. Personally, to me, it sounds like ones of those business idea myths that may have some bit of truth but it’s mostly a viral spin.

Surprising or not, AWS makes a lot of sense when you look at Amazons core competency. Logistics.

Look at any individual AWS service by itself, none of them are all that groundbreaking or innovative. What is groundbreaking is that Amazon has managed to take all of these services, and distribute them through a massively complex and infinitely scaling ecosystem. That’s logistics.

This is very true. I remember around 2005-06 when they publicized black Friday as a proof by fire of their technology, pretty much daring the internet to bring their site down with huge deals all at the same time. And it was amazing that their website kept working. After that it seems like they realized they could sell the idea of automatically, infinitely scaling infrastructure, but it wasn't at all obvious from the outside.

> What Amazon is great at is turning its own infrastructure needs into revenue instead of a cost

Let's hope that it decides to offset the cost of all those planes hauling its boxes around the country by selling tickets to paying passengers.

It could be Spirit Airlines, but without the terrible customer service, terrible conditions, and nickel-and-diming of its customers. All we want is a safe, reliable, solid, FAIRLY PRICED airline ticket.

Let's hope that it decides to offset the cost of all those planes hauling its boxes around the country by selling tickets to paying passengers.

I don't know how accurate this is, but a private jet pilot I was sitting next to on a flight told me that excess passenger airline baggage space was already being used to ship packages. If that's true, then baggage fees make a lot of sense. Passengers would be competing with Amazon and other companies for that space.

You are correct. It was government contracts to haul mail that turned flying airplanes into an industry back in the early days. Passenger service was added later.

Cargo remains more profitable than people even today. That's why you can still ship packages via passenger bus. Or at least you could the past time I did it in the early 2000's via Greyhound Package Express.

I'm not saying it Amazon Airlines should look like United, with a couple of hundred people up top and all the cargo down below. But maybe add 50 or 60 seats in a space in front.

One of the problems with cargo is that it's so ephemeral. A plane on a particular route can be full of packages at Christmas, and then half empty the rest of the year. This is exactly the sort of problem that Amazon seems good at solving.

Maybe make the passenger compartment modular. Add more seat modules when cargo loads are low. Add more cargo pods when demand is high.

But why? Passenger transport is already well catered for and extremely low margin. Also, passengers are annoying and generally not cardboard wrapped. They require seats and toilets and cabin attendants and pretzels and infant flotation devices. Cardboard boxes also don't videotape you when you offload them last minute to make room for something more valuable.

And that's before accounting for scheduling. Freight flights are often late nights, because cardboard boxes don't have eyes that can go red.

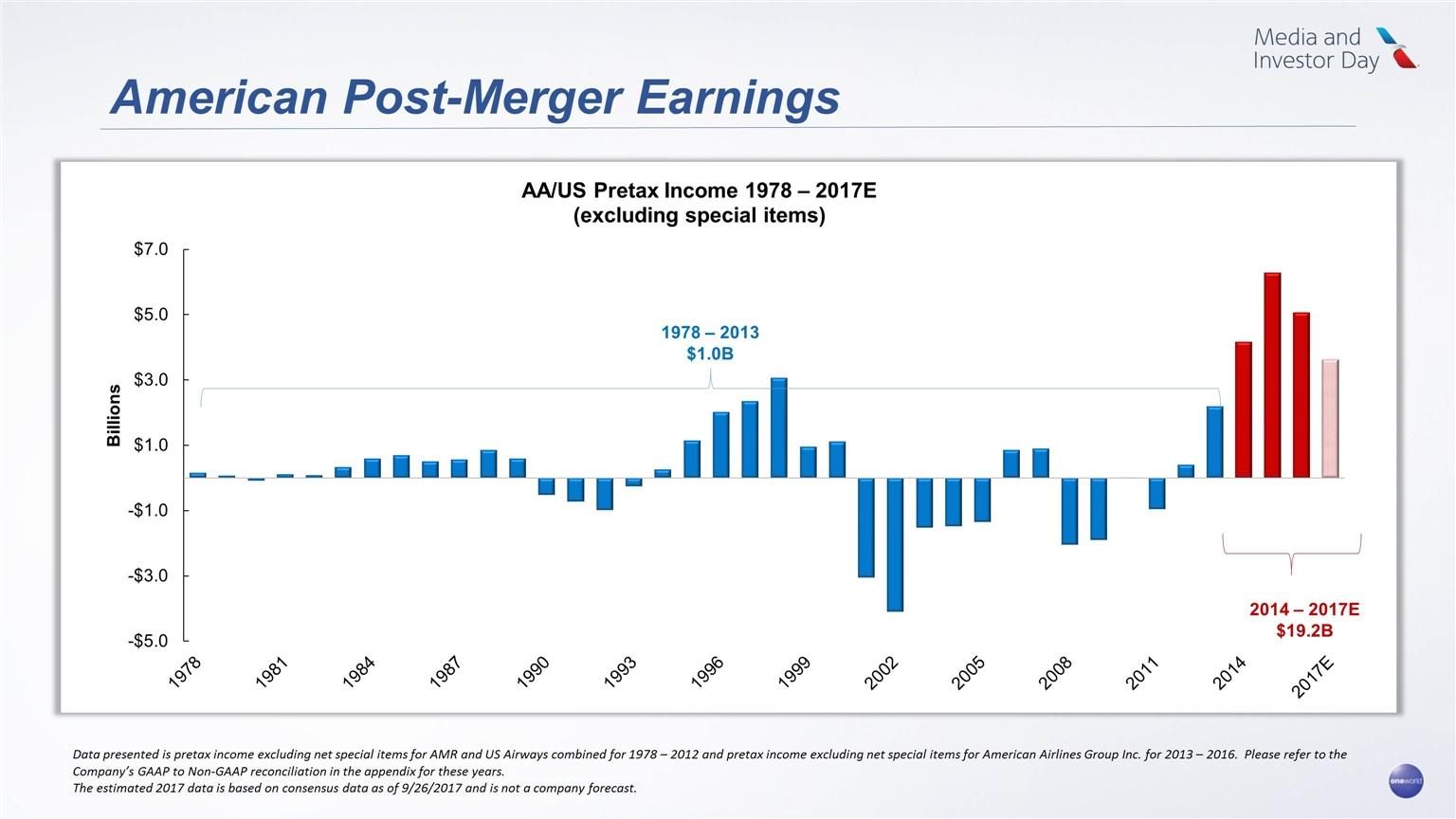

AA filed chapter 11 in 2011. They are doing well now, but they are very vulnerable to things they can't control well, like fuel prices, unions, etc.

In fact, the bankruptcy is part of why they are doing well now. It allowed them a free pass to invalidate all union contracts and start over with lots of leverage.

That $10B is a high number, certainly, but it's historically high. It's worth keeping context in mind here: this profit is earned on 446B passenger miles. Every time you fly a mile on AA, they profit a whopping 2.2 cents, and that's in historically good years. Even on a 7000 mile long-haul, that's just over $150 average per passenger. Devil's advocate says that smaller legroom is the reason they can turn a profit at all.

Low margin would be if they made $5. A $150 profit is pretty good since there are 200+ people in the plane. That's $30,000 a flight.

And remember, we're talking profit here, not income. I can't think of a scenario where a business with millions of paying customers would sneer at merely making a profit of $150 off of each one.

I'm not saying Amazon will switch to passenger transport, but you can imagine that their strategy would be to dominate the market by subsidizing ticket prices, then once they have the proper penetration, to raise ticket prices and be the first airline to increase margins in some time.

Anecdotally, I have never had an issue flying spirit and have done so on many occasions. They have a couple cheap direct flights from KC - Detroit/Chicago (family is right in between) and seasonally Portland - Detroit that are mega cheap

I had a Spirit flight to Charlotte that never took off. I ended up having to cancel my trip entirely. And the interwebs are full of Spirit horror stories.

Also, conventional wisdom is to not fly Spirit if you're of average height or above.

This made me look up flight maps. I have always hoped Spirit would start flying out of Charlotte. They have never operated here and still do not. Your experience may have been with Allegiant or Frontier (or flying to another city).

6'3" here and trust me Spirit is different than others. Knee to lower back/butt length didn't allow me to fully sit into the seat without wedging myself into it. It was not a pleasant experience but I was just a couple years out of college and heading to Miami for a football game so for $75 I dealt with it, but I've never flown on them again and were very happy that we had gotten a rental car to share driving back to Atlanta.

That said, they provide a great value and I have an aunt that used them extensively to be with me grandparents while their health was failing, so apart from being a terrible experience for tall people I’ve very glad they exist.

AWS was never an intention from the start. Some Amazonian in the mid 2000s saw the opportunity, wrote a three-pager about it, Jeff Bezos agreed, and now we have AWS.

I’d be interested in reading more about this. That employee changed Amazon’s future (and indeed the future of computing in general) immensely. I hope he/she was fairly compensated and relaxing on a beach far from Seattle now.

I wonder what the actual likelihood of that is. The stock has increased at least 20x since 2008, so, assuming the employee had options beginning in 2004, they could have made a decent amount of money off that.

Ideally if Google management wants to run these types of companies, they should pay dividend on the shares, taking money out and then invest in these businesses. The only reason I can think of for allowing Google management to throw other peolpe's money at their pet projects is taxes

The profits generated from Google's business belongs to the shareholders ( owners ) of the company. If the money can be used to defend the business ( Android, Chrome etc ) it can be - and should be - reinvested. Is self-driving cars related to search ? You could argue that it defends the brand. But otherwise, the money should be paid out as a divident and the cash thus obtained by Google's management ( Larry and Sergey still hold a lot of Google stock ) can be used to fund these type of projects. Other shareholders who do not believe in such projects can invest their dividents in businesses they believe in

That he came up with AWS tells us a lot about his acumen. Google reportedly has failed to build a viable rival although they had kubernetes in their internal system for a long time.

I would be skeptical. They conjured up profits when the analysts finally demanded it.

My guess is that Amazon will be the next big accounting scandal. I doubt anyone truly understands how the company works.

AWS has a big head start, but the margins aren’t going to last as Microsoft and Google grow. Once one of them decide to buy the business by slashing network costs, poof.

I dunno. Depends on how rapidly folks move away from AWS to other clouds. And that to some extent depends on lock in.

If all you are doing on AWS is ec2/vpc, moving to gcp is pretty easy. But if you are leveraging any of the proprietary tech like kinesis, lambda or sqs, it's going to take an application rewrite. Which means that it will have to be a very compelling price break. I don't have a good feeling for what the product penetration is for non IAAS services is.

Now, for green field development, where there's no legacy AWS integration, pricing becomes a lot more important.

> “Cost center” doesn’t mean “unprofitable department”.

That's unnecessarily pedantic. A cost center is an organizational subunit that incurs cost but does not directly contribute to the company’s profits. Since I said "department" and "cost center" it really should be clear what was meant. Why, it is just like the article itself using "Amazon" as both a noun and a verb!

> And actually two of the three segments appearing in Amazon financial reports are profitable.

Amazon had 6 segments in 2017 not 3.

If you look at the Operating Profit, Operating Margin, and P/E considering the context of my comment about AWS vs. the other departments, I think you will see why AWS has kept Amazon (and AMZN) afloat.

{kind=link}

Selling books to selling computing on demand... That was a big leap, and the most profit generating "pivot" I can think of.

Alexa, video streaming, kindle and ono...these are really Amazon becoming like Google. They're now defined as a business by the skills/abilities they have, not the services they provide. Technology company, not search company.

..this justifies investing more on self driving cars or nuclear power and less on search engines. For most companies this would just be pr/hr-speak, and impossible in practice. Usually companies have to spend most of their money on core products, because it takes money to deliver those products. Tesla or Walmart could define themselves however they want, but they'll never be able to spare more than a penny or two of car dollars on stuff that isn't related to making cars. The margin isn't there.

To be a Google, you need a legitimate cash cow. Amazon now have one, aws.